Insurance industry astroturfer urges voters to reject Referendum 67 in letter

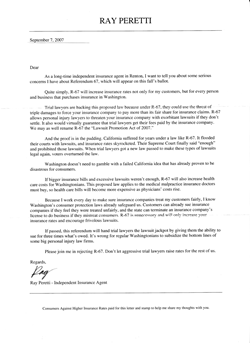

Last Friday, I received a letter from an "independent insurance agent" named Ray Peretti, who is actually an industry lobbyist, warning me about the allegedly terrible consequences should Referendum 67 pass. From what I can gather, many registered voters all over my area also received this letter. (You can read a scan of that letter here. )

Suffice it to say, for starters, that Peretti is not very independent. It's a campaign letter, if you read the incomplete disclosure at the bottom of the page. (Note to Ray: check with the PDC on how to do a proper disclosure.)

The campaign group "Consumers Against Higher Insurance Rates" has nothing to do with consumers and is simply a front group for the insurance industry.

The campaign group "Consumers Against Higher Insurance Rates" has nothing to do with consumers and is simply a front group for the insurance industry.

The key reform contained in Referendum 67 is that consumers could sue for up to triple damages when they are denied payment on a legitimate claim, which the Legislature determined would be a reasonable consumer protection.

Right now consumers are virtually defenseless against insurance company abuse, because even if a consumer goes to court and wins 100% of what is owed them, they still have to pay legal expenses.

Last month Olympian reporter Brad Shannon detailed the tremendous sums of cash the insurance industry is throwing into the state campaign against R-67, and he also quoted an attorney (gasp!) who neatly summarized the heart of the matter:

The first thing one finds out upon Googling Ray Peretti is that he was president of the PIA, the National Association of Professional Insurance Agents, and he had this to say at the beginning of his term in 2005. From the PIA web site:

Leaving that aside, what about the claims Peretti makes? Unsurprisingly, the letter is full of half-baked conclusions and misleading right-wing corporatist gibberish.

Lawyer-baiting is so wide-spread and well, dumb, that you would think it would no longer be a viable tactic. But not to Peretti. It's hard not to imagine a ballroom full of these insurance guys and gals, laughing at how they will stick it to those darn lawyers once and for all, and if a few "Grandma Millies" pay the price, oh well. Just the cost of doing business.

While Peretti's childish attempt at humor when he chortles that R-67 should be re-named "The Lawsuit Promotion Act of 2007" may resonate with some conservatives, it's probably not so funny to people who have had their home destroyed and may not be made whole even after taking the insurance companies to court. The campaign against R-67 is clearly an attempt to make sure a basic consumer protection is gutted.

But what about California? Didn't they have a bad experience?

Peretti clearly suggests that is the case, but unfortunately, he plays extremely loose with the facts. The "Reject R-67" campaign seems to be repeatedly referencing Proposition 103, a 1980's measure that sought to roll back insurance rates. From the California Department of Insurance:

While I'd agree that insurance law is hardly a scintillating reading topic, does Peretti have to slant every single point he makes with distortions?

The Proposition 103 Resource page from The Foundation for Taxpayer and Consumer Rights (FTCR) details the many consumer protections the measure offered, and in what could be taken as a warning to the citizens of other states, offers this little tidbit:

According to a fact sheet put out by the pro-consumer Approve 67 campaign, the industry knows it is spouting baloney and has been told so by some very knowledgeable people right here in Washington state:

But that's only true if one believes the industry's specious claim that there will be a flood of lawsuits, because R-67 doesn't regulate rates. From the FAQ section of the Approve 67 web site:

The triple damages would have to be imposed by a court of law, so the insurance industry's arguments are substantially without merit. In those cases where courts find that industry conduct is so egregious as to warrant damages, then our system of justice allows every member of society their fair day in court, not just corporations with pockets deep enough to fend off ordinary folks.

Don't be fooled: make sure to support R-67 by urging your friends and co-workers to vote "Yes" to keep these basic consumer protections on the books.

Washingtonians are usually smart enough not to be fooled by blatant corporate power grabs, and we have every reason to believe our citizens won't fall for insurance industry tricks this fall.

Suffice it to say, for starters, that Peretti is not very independent. It's a campaign letter, if you read the incomplete disclosure at the bottom of the page. (Note to Ray: check with the PDC on how to do a proper disclosure.)

The campaign group "Consumers Against Higher Insurance Rates" has nothing to do with consumers and is simply a front group for the insurance industry.

The campaign group "Consumers Against Higher Insurance Rates" has nothing to do with consumers and is simply a front group for the insurance industry.The key reform contained in Referendum 67 is that consumers could sue for up to triple damages when they are denied payment on a legitimate claim, which the Legislature determined would be a reasonable consumer protection.

Right now consumers are virtually defenseless against insurance company abuse, because even if a consumer goes to court and wins 100% of what is owed them, they still have to pay legal expenses.

Last month Olympian reporter Brad Shannon detailed the tremendous sums of cash the insurance industry is throwing into the state campaign against R-67, and he also quoted an attorney (gasp!) who neatly summarized the heart of the matter:

At issue with Referendum 67 is Senate Bill 5726, which Democrat-led legislators approved this year as a consumer protection measure. The bill authorizes consumers to sue for up to triple damages for denied legitimate claims in the area of fire, home, auto, long-term care and other non-medical insurance not covered by the state’s patient bill of rights law, said trial lawyer lobbyist Larry Shannon, who spoke at a forum on ballot measures last week in Lacey.The horror stories about insurance companies in the aftermath of Katrina are numerous and should serve as a warning to those of us out here in earthquake country--the insurance companies, in many cases, will simply not pay legitimate claims and they need to be held accountable. When an industry won't even pay the claims of a Republican senator you know something is amiss.

Shannon said the law is needed because consumers cannot be made whole when trying to force insurers to pay what they owe.

Although a person can sue an insurer for nonpayment, there is no incentive for insurers to pay because a consumer can only recover the amount owed under the claim — from which legal costs are deducted.

The first thing one finds out upon Googling Ray Peretti is that he was president of the PIA, the National Association of Professional Insurance Agents, and he had this to say at the beginning of his term in 2005. From the PIA web site:

“I’m from Washington, and I’m here to help you,” Peretti jokingly told his fellow agents and board members from around the country who gathered in September in Portland, Oregon to officially install him on September 11, 2005. “But don’t worry,” he hastened to add, “I’m from the other Washington. The one on the Potomac where the government spends our money that it doesn’t have — that’s the Washington PIA has to keep an eye on.”So while Peretti's letter gives the impression he is just a concerned local agent, he is in fact an industry flack-lobbyist with a decidedly conservative bent, at least judging from what he and his insurance pals find amusing. The PIA has recently joined the campaign against R-67, according to an industry newsletter web site.

Leaving that aside, what about the claims Peretti makes? Unsurprisingly, the letter is full of half-baked conclusions and misleading right-wing corporatist gibberish.

Lawyer-baiting is so wide-spread and well, dumb, that you would think it would no longer be a viable tactic. But not to Peretti. It's hard not to imagine a ballroom full of these insurance guys and gals, laughing at how they will stick it to those darn lawyers once and for all, and if a few "Grandma Millies" pay the price, oh well. Just the cost of doing business.

While Peretti's childish attempt at humor when he chortles that R-67 should be re-named "The Lawsuit Promotion Act of 2007" may resonate with some conservatives, it's probably not so funny to people who have had their home destroyed and may not be made whole even after taking the insurance companies to court. The campaign against R-67 is clearly an attempt to make sure a basic consumer protection is gutted.

But what about California? Didn't they have a bad experience?

Peretti clearly suggests that is the case, but unfortunately, he plays extremely loose with the facts. The "Reject R-67" campaign seems to be repeatedly referencing Proposition 103, a 1980's measure that sought to roll back insurance rates. From the California Department of Insurance:

Proposition 103 (Section 1861.01 (a) of the California Insurance Code (CIC)) required that every insurer reduce its rates to at least 20% less than the rates that were in effect on November 8, 1987 unless such rollback would lead to a company's insolvency. This provision was later changed by the California Supreme Court to allow companies a fair rate of return. Since 1989, the Rate Regulation Division has been responsible for negotiating with insurance companies to meet their rollback obligations.So while it's true that the California Supreme Court, in effect, changed Prop. 103, there's more to the story than that.

While I'd agree that insurance law is hardly a scintillating reading topic, does Peretti have to slant every single point he makes with distortions?

The Proposition 103 Resource page from The Foundation for Taxpayer and Consumer Rights (FTCR) details the many consumer protections the measure offered, and in what could be taken as a warning to the citizens of other states, offers this little tidbit:

* THE LEGISLATURE AND PROP. 103. The Legislature is not allowed to rewrite Proposition 103 in any way that undermines its protections.So Prop. 103 was only a "disaster" because the insurance industry has never stopped trying to make it one. Big surprise.

Proposition 103 was necessary because the California Legislature was too beholden to the insurance industry and refused to pass needed reforms. To protect itself against the insurance lobby once it became law, Proposition 103 specifically prohibits the Legislature from hostile amendments. That hasn't stopped the Legislature from trying, though.

According to a fact sheet put out by the pro-consumer Approve 67 campaign, the industry knows it is spouting baloney and has been told so by some very knowledgeable people right here in Washington state:

The same insurance industry lobbyists and executives who are paying for this campaign know that this is deceptive. They were forced to admit in front of Washington’s Legislature that this bill has nothing to do with the California experience and were directed by committee chairs in the House and Senate to abandon this argument because it is patently false. Once more, the California law actually stabilized premiums three years before the law in question was overturned.The Peretti letter claims repeatedly that R-67 will raise insurance rates, which naturally is what the insurance industry wants people to believe.

But that's only true if one believes the industry's specious claim that there will be a flood of lawsuits, because R-67 doesn't regulate rates. From the FAQ section of the Approve 67 web site:

Will Referendum 67 increase my insurance premiums?It's important to understand that insurance companies have nothing to fear, and rates can't be raised, if the industry pays legitimate claims. In other words, follow the law like the rest of us.

No. Referendum 67 does not address insurance premiums in any way. Insurance premiums in Washington have consistently risen and fallen with the market. In fact, the insurance industry continues to be one of the most profitable industries in the state and nation, as profits have skyrocketed to record highs in the last two years.

The triple damages would have to be imposed by a court of law, so the insurance industry's arguments are substantially without merit. In those cases where courts find that industry conduct is so egregious as to warrant damages, then our system of justice allows every member of society their fair day in court, not just corporations with pockets deep enough to fend off ordinary folks.

Don't be fooled: make sure to support R-67 by urging your friends and co-workers to vote "Yes" to keep these basic consumer protections on the books.

Washingtonians are usually smart enough not to be fooled by blatant corporate power grabs, and we have every reason to believe our citizens won't fall for insurance industry tricks this fall.

{kind=link}